Understanding Seasonality in Car Shipping: Pricing Waves & Demand Cycles

Understanding Seasonality in Car Shipping: Pricing Waves & Demand Cycles

Car shipping in the United States operates much like any other logistics-heavy industry — it moves in cycles. Rates rise and fall throughout the year, driven by migration trends, weather patterns, auction schedules, and vehicle sales. Whether you’re a shipper, broker, or carrier, understanding these seasonality patterns is key to quoting accurately, protecting margins, and delivering a smoother customer experience.

This guide breaks down how seasonality affects car transport pricing, what typically happens in each quarter, where regional differences matter, and how modern, industry-focused tools help professionals stay ahead of these waves instead of chasing them.

1. Why Seasonality Matters in Car Shipping

Car transport is not just about moving vehicles from point A to point B; it’s about anticipating demand. Brokers who understand the seasonal rhythm can quote with confidence, set realistic expectations, and build stronger relationships with both customers and carriers. Those who ignore it risk losing profit when rates spike, or disappointing customers when trucks aren’t available at the price they promised.

Several consistent forces drive the seasonal waves in car shipping: snowbird migration, auto sales volume, weather events, moving season, and auction cycles. When these overlap, lanes tighten and prices climb. When they cool down, competition for loads increases and prices become more flexible.

Factor | Impact on Car Shipping Demand | Typical Months |

|---|---|---|

Snowbird Migration | Sharp two-way demand between North and South as retirees move with the seasons. | Oct–Dec (Southbound), Apr–May (Northbound) |

Auto Sales Volume | Inventory cycles and incentives drive dealer and OEM shipping volume. | Year-round, peaks in Q2–Q3 |

Weather Events | Hurricanes, snowstorms, and flooding disrupt routes and create urgent shipments. | Aug–Nov (Hurricanes), Jan–Feb (Winter storms) |

Moving Season | Relocations and multi-vehicle family moves intensify demand. | May–Sept |

Auction Cycles | Wholesale and dealer auctions shift truck capacity toward key corridors. | Feb–Mar, Sept–Nov |

2. The Annual Cycle: Quarter-by-Quarter Breakdown

Each part of the year shapes pricing and carrier availability differently. Recognizing these patterns transforms guesswork into strategy for brokers and carriers alike.

Q1: The Post-Holiday Dip (January–March)

Demand: low to moderate | Rates: stable or decreasing | Carrier availability: high

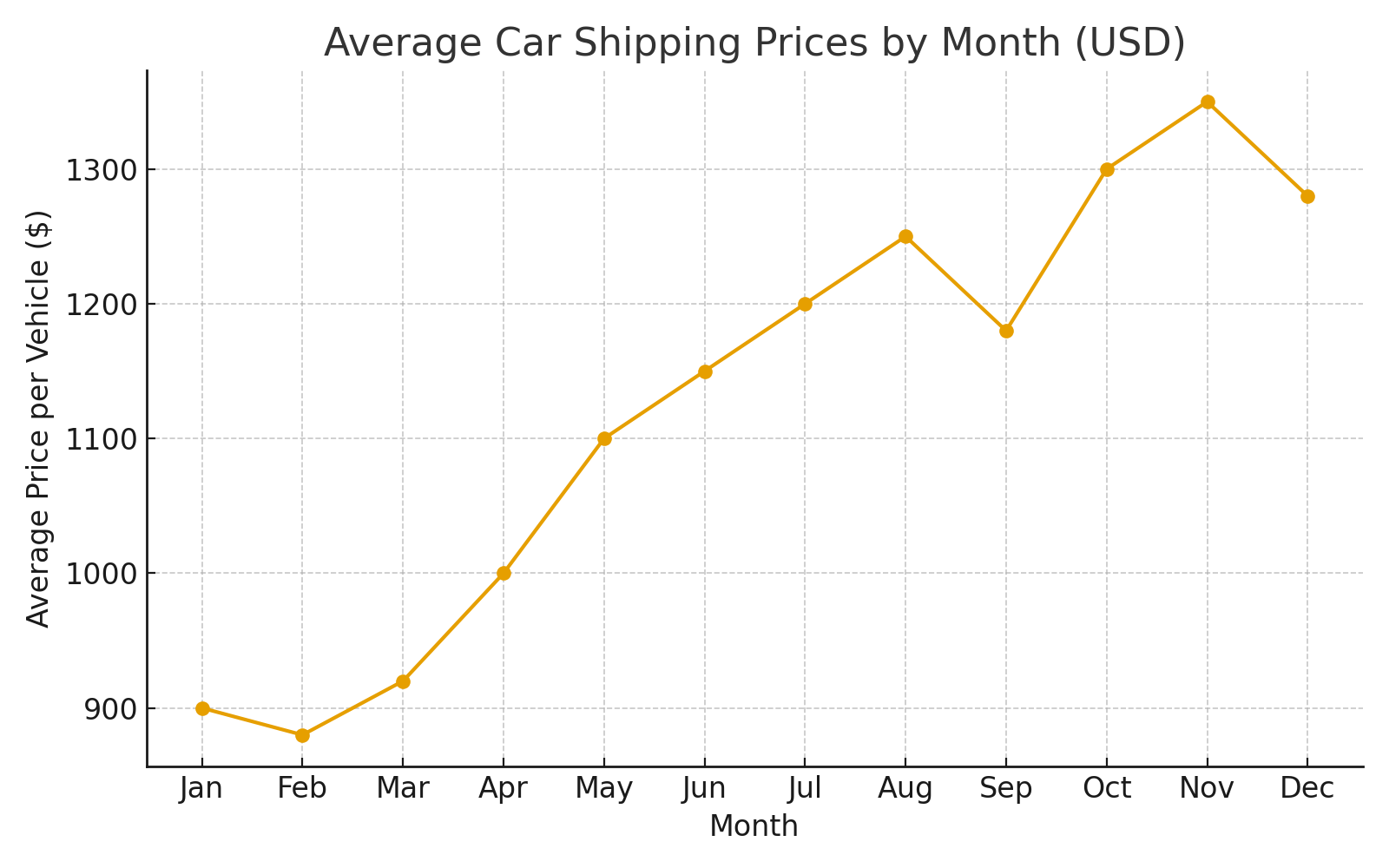

After the holidays, most southbound snowbirds are already in place, and dealership movements cool down. Carriers often compete for loads, which pushes prices downward and makes this one of the best windows for budget-conscious shippers. A sedan from Chicago to Miami in January might average around $850, compared to $1,050+ in October on the same lane.

Q2: Spring Rebound (April–June)

Demand: rising | Rates: increasing | Carrier availability: tightening

As temperatures climb, snowbirds return north, relocations pick up, and dealers restock lots. This creates strong northbound demand and occasional lane imbalances. Brokers that monitor market data and adjust quotes proactively stay ahead of sudden spikes instead of apologizing for them.

Q3: The Summer Surge (July–September)

Demand: high | Rates: moderate but volatile | Carrier availability: limited

Summer is classic moving season: families relocate, students change states, and corporate transfers kick in. Capacity is tight, and fuel price swings can trigger short-lived but sharp rate increases. A Dallas-to-Seattle shipment, for example, may climb from roughly $1,200 in June to $1,450 in August due purely to capacity squeeze and fuel fluctuations.

Q4: The Snowbird Season (October–December)

Demand: very high (especially southbound) | Rates: peak | Carrier availability: extremely limited

This is the busiest stretch of the year on lanes like New York → Florida, Midwest → Arizona, and Northeast → Texas. Southbound demand surges while northbound freight often trades at a discount. It’s common to see New York → Florida pricing in the $1,200–$1,500 range while the reverse lane is hundreds less. Brokers who pre-book carriers, lean on automation, and communicate early protect both margins and reputation.

Figure 1: Illustrative average car shipping prices by month, highlighting seasonal peaks and dips.

3. Regional Differences in Demand Waves

Not every region behaves the same way. Some are heavily influenced by retirees, others by tech hubs, ports, or harsh winters. Recognizing these nuances helps brokers propose better timing, alternate routes, or flexible delivery windows instead of forcing every shipment into the same template.

Region | Seasonal Demand Pattern | Key Routes |

|---|---|---|

Northeast | Strong southbound in fall and northbound in spring driven by snowbirds and relocations. | NY–FL, NJ–TX |

Midwest | Weather-sensitive with steady dealer and auction flows. | IL–CA, MI–TX |

South | Consistent year-round activity, boosted by winter inflows. | FL–NY, TX–CA |

West Coast | Balanced lanes driven by relocations, ports, and tech migration. | CA–WA, CA–AZ |

Mountain States | More limited volume; winter weather can force longer routes. | CO–CA, NV–TX |

4. Data Snapshot: U.S. Car Shipping Volume by Season

While exact numbers fluctuate year to year and by data source, the relationship between seasonal demand and pricing is consistent: when volume climbs, available capacity tightens and prices follow. The simplified snapshot below illustrates how quarterly averages often align.

Quarter | Avg. Monthly Shipments (Est.) | Avg. Price per Vehicle (Est.) | Notes |

|---|---|---|---|

Q1 | 240,000 | $900 | Post-holiday dip; more open capacity and competitive rates. |

Q2 | 310,000 | $1,050 | Spring rebound driven by returns, moves, and auctions. |

Q3 | 350,000 | $1,150 | Peak moving season; tight capacity and occasional fuel surcharges. |

Q4 | 420,000 | $1,300 | Snowbird season; strong southbound demand and premium pricing. |

Figure 2: Illustrative relationship between seasonal shipment volume and average pricing by quarter.

5. How Brokers and Carriers Can Leverage Seasonal Trends

For brokers:

Pre-book carriers for key lanes ahead of peak months.

Use dynamic quoting tied to current market signals, not outdated rate sheets.

Educate customers early about busy seasons and realistic timelines.

Diversify routes and customers so you’re not dependent on a single seasonal pattern.

For carriers:

Plan return loads to reduce deadhead miles on seasonal corridors.

Watch fuel and weather trends and adjust rates before they erode margins.

Leverage digital platforms and integrations to fill gaps quickly with quality freight.

6. The Role of Technology and Automation

In the past, managing these waves meant phone calls, sticky notes, and spreadsheets. Today, modern auto transport platforms quietly do the heavy lifting in the background: pulling in signals from load boards, historical rates, fuel indexes, and regional demand to support more precise pricing and better timing.

Brokers using integrated CRMs built specifically for auto transport can:

See real-time visibility into lane performance and carrier availability.

Automate quote follow-ups around seasonal peaks.

Keep all communication, orders, and analytics in one connected view.

That kind of infrastructure allows even lean brokerages to operate with enterprise-level discipline: consistent pricing logic, fewer missed opportunities, and a calmer experience for everyone involved. The platforms that get this right don’t just send emails; they help teams think in seasons, not single shipments.

7. Looking Ahead: Smarter Seasonal Forecasting

As more data flows through the industry, seasonal forecasting will only get sharper. Patterns like snowbird surges, Sun Belt migration, EV movements, and regional weather disruptions are increasingly measurable rather than anecdotal. Seasonality won’t disappear, but its impact becomes far more manageable when it’s visible.

Conclusion

Seasonality in car shipping isn’t a mystery; it’s a pattern waiting to be mastered. By understanding how migration, weather, auctions, and relocation cycles shape demand, brokers and carriers can quote smarter, book earlier, and protect both customer trust and profitability.

The real advantage going forward won’t be simply knowing that October is busy or January is slow — everyone in the market knows that. It will belong to the teams that use the right tools and data to anticipate those waves, adjust in real time, and turn seasonal volatility into a competitive edge.